Now that my roaring twenties are behind me, I’ve been getting a lot more serious about my hard-earned cash money. Gone are the days when I would spend afternoons digging through fashion blogs looking at the chronology of Nicole Richie’s style evolution or seeking out the best online deals on Marc by Marc Jacobs purses. These days, the bulk of my free time on the web is spent comparing credit card rates and scouring MSL listings for hidden gems. Adulting, amiright?

So when an email from LowestRates.ca landed in my inbox urging me to buy fancy coffees and treat myself to manicures in favour of saving money, I was very intrigued.

The Canadian personal finance comparison site wants us to forget about “The Latte Factor,” a popular penny-pinching strategy. Instead, they want us to focus on saving money on the BIG expenses and indulging in the small stuff where it counts. After all, living frugally is no fun.

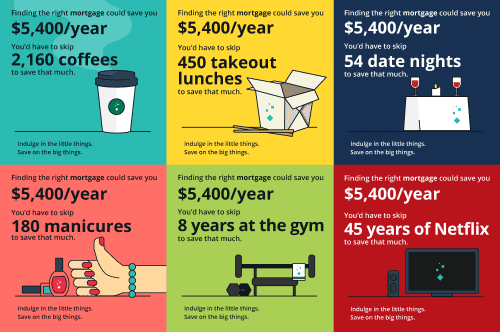

DYK that finding the right mortgage could save you up to $5,400 per year, meaning you’re free to #treatyoself to:

- 2,160 takeout coffees ($2.50 per coffee)

- 450 takeout lunches ($12 per lunch)

- 54 date nights ($100 per date night)

- 180 manicures ($30 per manicure)

- 8 years at the gym ($675 membership per year)

- 45 years of Netflix ($120 subscription per year)

We had the opportunity to chat about financial planning and mortgage rates with Justin Thouin, CEO of LowestRates.

For those of us who aren’t finance-literate, can you explain in layman’s terms what LowestRates.ca is all about?

LowestRates.ca is all about providing Canadians with options for the personal finance products they need, such as insurance, mortgages, and credit cards. It works like Expedia: you go to one place and compare prices from multiple companies. The only difference is that, unlike shopping for flights or hotels, comparing options for personal finance can save you serious money – up to thousands of dollars a year.

What’s the biggest misconception Canadians have about mortgage rates?

That you don’t have options and you just have to accept what your bank offers. Not only do the mortgage rates you get from banks when you just walk in tend to be higher than if you shop around, but it’s also faster and easier to find a mortgage through a rate comparison site like LowestRates.ca.

When it comes to saving money, I’ve always heard that cutting back on the smaller expenses that goes the longest way. Can you explain why this may be a flawed way of thinking?

It’s flawed simply because you can save much more – and much more easily – by looking at the big expenses in life. Sure, cutting back on to-go coffees and takeout food will save you money, but nothing compared to getting a lower mortgage rate or reducing your monthly auto premium or credit card interest payments. We tend to look at the small things and ignore the big stuff – it’s called being “penny-wise, pound-foolish.” So we say enjoy your morning coffee, but make sure you compare your options when it comes to the big financial decisions.

It’s shocking how many people in their twenties and thirties still depend on their parents for help with money matters like income taxes, loans, etc. What are some resources millennials can use to educate themselves and to learn how to manage their finances?

Many Canadians – both young and old – have never been properly taught about finance, so they end up following in the footprints of their parents – a habit that can be quite costly. We believe strongly in educating people to make the smartest financial decision for their unique situation, which is why we publish daily tips, stories, and insights from some of Canada’s leading voices in personal finance. There are also some great Toronto-based personal finance bloggers out there, such as Jessica Moorhouse’s Mo’ Money Podcast and Barry Choi’s Money We Have, and the Globe and Mail has a ongoing Gen Y Money series.

It’s all about empowerment. And remember, you don’t have to be a money expert to make smart financial decisions.

For more info, you can visit the LowestRates.ca blog post here.